The home appraisal process is a crucial part of most real estate transactions. Whether you're buying or selling a property in San Francisco, knowing what to expect during the appraisal can help you prepare, respond strategically, and keep the deal on track.

In competitive markets like San Francisco—where historic homes, mixed-use properties, and variable neighborhood pricing are common—appraisals are more than routine. They influence financing, negotiations, and even whether a transaction moves forward. Understanding each stage of the process helps you approach this step with confidence and clarity.

What Is a Home Appraisal and Why It Matters

A home appraisal is a professional opinion of a property's market value. For financed transactions, lenders require appraisals to confirm that the property is worth at least the amount being borrowed. For sellers, an appraisal can either support the agreed-upon price or introduce complications if it comes in low.

In San Francisco, where property values shift quickly and homes often include custom renovations, appraisers must evaluate a range of factors. These include the condition of the home, recent comparable sales, and local market activity.

The outcome of the appraisal can impact whether the buyer's loan is approved, whether additional negotiations are necessary, or whether the deal continues as planned. That's why both parties should be ready for what comes next.

In San Francisco, where property values shift quickly and homes often include custom renovations, appraisers must evaluate a range of factors. These include the condition of the home, recent comparable sales, and local market activity.

The outcome of the appraisal can impact whether the buyer's loan is approved, whether additional negotiations are necessary, or whether the deal continues as planned. That's why both parties should be ready for what comes next.

Who Orders the Appraisal and When It Happens

After a buyer’s offer is accepted, their lender typically orders the appraisal. This usually happens early in the escrow period, once the initial contingencies are addressed. The appraiser is selected by a third-party appraisal management company to maintain independence and objectivity.

The appraiser will contact the listing agent to schedule a visit to the property. In most cases, the inspection itself takes 30 to 60 minutes. The appraiser then spends additional time analyzing market data and preparing the report. In San Francisco, appraisal reports often require deeper research due to variations in property types, zoning, and historic overlays.

The final appraisal report is generally delivered within one to two weeks. If you’re buying with financing, your lender will share the result and let you know whether the value supports the loan amount.

The appraiser will contact the listing agent to schedule a visit to the property. In most cases, the inspection itself takes 30 to 60 minutes. The appraiser then spends additional time analyzing market data and preparing the report. In San Francisco, appraisal reports often require deeper research due to variations in property types, zoning, and historic overlays.

The final appraisal report is generally delivered within one to two weeks. If you’re buying with financing, your lender will share the result and let you know whether the value supports the loan amount.

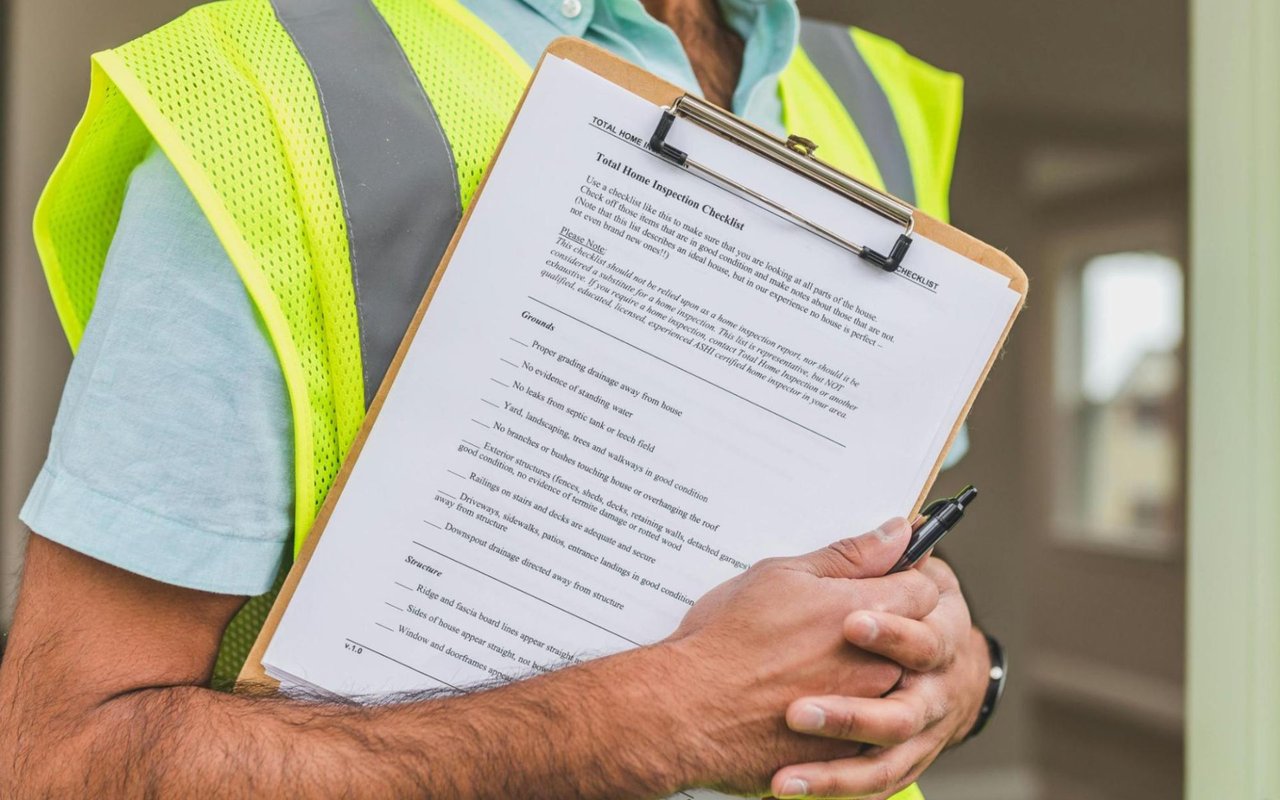

What Appraisers Look For During the Visit

Appraisers follow a consistent process, but the property itself can affect how they evaluate its value. During the visit, the appraiser will:

-

Measure the square footage and confirm the layout matches public records

-

Assess the property’s condition, including visible upgrades or deferred maintenance

-

Document interior and exterior features, like flooring, appliances, landscaping, and structural systems

-

Take photographs of every major room and any special features or improvements

While appraisers do not perform full inspections, they will note visible concerns that could affect value or marketability. In San Francisco, older homes may raise questions about foundation integrity, outdated systems, or the quality of renovations.

Once the site visit is complete, the appraiser will turn to comparable sales. These are recently sold properties in the same area that are similar in size, age, and condition. The appraiser will adjust values to account for any differences between the subject property and those comps.

Once the site visit is complete, the appraiser will turn to comparable sales. These are recently sold properties in the same area that are similar in size, age, and condition. The appraiser will adjust values to account for any differences between the subject property and those comps.

How San Francisco Properties Affect Appraisals

San Francisco’s housing stock includes a wide range of architectural styles, lot sizes, and building types. As a result, appraisals in the city can be more complex than in newer suburban areas.

Victorian homes, for example, may have features that are difficult to quantify in a standard report. A well-maintained facade, restored woodwork, or period-specific upgrades may contribute to value, but not all appraisers assign equal weight to these elements.

Multi-unit buildings, tenant-occupied properties, and mixed-use zoning also require specialized knowledge. In these cases, appraisers must factor in rental income, long-term tenancy restrictions, or land-use regulations, which can influence both desirability and appraised value.

Victorian homes, for example, may have features that are difficult to quantify in a standard report. A well-maintained facade, restored woodwork, or period-specific upgrades may contribute to value, but not all appraisers assign equal weight to these elements.

Multi-unit buildings, tenant-occupied properties, and mixed-use zoning also require specialized knowledge. In these cases, appraisers must factor in rental income, long-term tenancy restrictions, or land-use regulations, which can influence both desirability and appraised value.

What Happens If the Appraisal Comes in Low

An appraisal that meets or exceeds the purchase price allows the transaction to move forward as planned. But if the appraised value is lower than the agreed price, the deal may need to be renegotiated.

Here are your options if an appraisal comes in low:

-

The buyer can make up the difference with additional funds

-

The seller can agree to lower the purchase price to match the appraised value

-

Both parties can negotiate a compromise between price and out-of-pocket costs

-

The buyer can dispute the appraisal through the lender, providing additional comps

-

The buyer can cancel the contract if an appraisal contingency is in place

In a competitive market, it’s not uncommon for properties to sell above appraised value. Buyers and sellers should be prepared to respond quickly if this occurs. Working with an experienced agent can help determine whether to push forward, renegotiate, or walk away.

Tips to Prepare for a Successful Appraisal

Whether you're the buyer or the seller, you can play a role in making sure the appraisal goes smoothly.

For sellers:

-

Clean and declutter the home before the appraisal visit

-

Make a list of recent upgrades or repairs, including dates and costs

-

Provide access to all areas of the home, including garages, basements, and outbuildings

-

Share any permits or plans for major renovations

For buyers:

-

Stay in contact with your lender and respond promptly to document requests

-

Let your agent know as soon as the appraisal is scheduled

-

Be ready to discuss next steps if the value doesn’t match the purchase price

A well-prepared appraisal visit, backed by accurate data and strong communication, helps keep the process on track and avoids unnecessary surprises.

What to Expect After the Appraisal

Once the appraisal report is delivered, the lender will review it and confirm whether the value supports the loan. If all looks good, the transaction moves forward. If there are issues, you’ll receive guidance on next steps.

For buyers, this may mean deciding how to handle a value gap. For sellers, it could mean reopening price discussions or gathering more data to support the original number.

In either case, staying responsive and flexible during this stage helps prevent delays and increases the odds of a smooth closing.

For buyers, this may mean deciding how to handle a value gap. For sellers, it could mean reopening price discussions or gathering more data to support the original number.

In either case, staying responsive and flexible during this stage helps prevent delays and increases the odds of a smooth closing.

Reach Out to Bonnie Spindler

When you’re buying or selling in San Francisco, working with an agent who understands the home appraisal process can make all the difference. Bonnie Spindler brings extensive experience with historic properties, financing timelines, and valuation trends unique to the city. She helps clients prepare for appraisals, respond effectively to low values, and keep transactions moving.

Bonnie’s expertise includes managing appraisals for single-family homes, multi-unit buildings, and mixed-use properties across San Francisco. Whether you're concerned about comps, timing, or how to present a property, Bonnie is ready to help you navigate every step. Contact Bonnie Spindler today to receive guidance rooted in market knowledge and focused entirely on your success.

Bonnie’s expertise includes managing appraisals for single-family homes, multi-unit buildings, and mixed-use properties across San Francisco. Whether you're concerned about comps, timing, or how to present a property, Bonnie is ready to help you navigate every step. Contact Bonnie Spindler today to receive guidance rooted in market knowledge and focused entirely on your success.